Kripto paraların Python ile kolerasyonlarını inceleme

01 Feb 2022

Detayları ile anlattığım videonun LINK. Bununla birlikte kodun da LINK

Kodun örnek yansısı

from binance import Client

binance_cli = Client(API_KEY, API_SECRET)

tickers = binance_cli.get_exchange_info()

tickers = [a["symbol"] for a in tickers["symbols"]]

usdtPairs = []

btcPairs = []

exclude = ["DOWN", "UP", "BULL", "BEAR", "YEN", "TRY", "EURO", "EUR", "TUSD", "BUSD", "USDC", "USDS"]

for ticker in tickers:

if ticker.endswith("USDT") and all(element not in ticker for element in exclude):

usdtPairs.append(ticker)

elif ticker.endswith("BTC"):

btcPairs.append(ticker)

usdtPairs

import pandas as pd

"""

[

1499040000000, # Open time

"0.01634790", # Open

"0.80000000", # High

"0.01575800", # Low

"0.01577100", # Close

"148976.11427815", # Volume

1499644799999, # Close time

"2434.19055334", # Quote asset volume

308, # Number of trades

"1756.87402397", # Taker buy base asset volume

"28.46694368", # Taker buy quote asset volume

"17928899.62484339" # Can be ignored

]

"""

binance_cli.get_klines(symbol = "BTCUSDT" , interval = '4h', limit = 10 )

def getData(symbol ,interval = "4h", limit = 10):

subFrame = pd.DataFrame(binance_cli.get_klines(symbol = symbol , interval = interval, limit = limit ))

subFrame = subFrame.iloc[:, :6]

subFrame.columns = ["Time", "Open", "High", "Low", "Close", "Volume"]

subFrame = subFrame.set_index("Time")

subFrame.index = pd.to_datetime(subFrame.index, unit="ms")

subFrame = subFrame.astype(float)

return subFrame

arr = []

for pair in usdtPairs[0:50]:

df = getData(pair)

print("Getting Klines for", pair)

arr.append(getData(pair))

dict(zip(usdtPairs[0:50], arr))

df = pd.concat(dict(zip(usdtPairs[0:20], arr)), axis=1)

closedf = df.loc[:, df.columns.get_level_values(1).isin(["Close"])]

closedf.columns = closedf.columns.droplevel(1)

closedf = closedf[closedf.iloc[-1].dropna().index].dropna()

closedf

import numpy as np

"""# Log return formula

log(percentage change + 1) -> (log is a natural logarithm)

OR

log(final element / initial element) -> (log is a natural logarithm)

## Cumulative Return

exp(sum(all log returns)) - 1

"""

example = pd.Series(np.random.randint(1,5,5))

example.pct_change()

print(np.log(example.pct_change()[2] + 1), np.log(example[2] / example[1]), np.exp(sum(np.log(example.pct_change()[1::] + 1))) - 1)

np.expm1(sum(np.log(example.pct_change()[1::] + 1)))

log_df = np.log(closedf.pct_change() + 1)

log_df.drop(closedf.index[0], inplace=True)

log_df

log_df.corr()

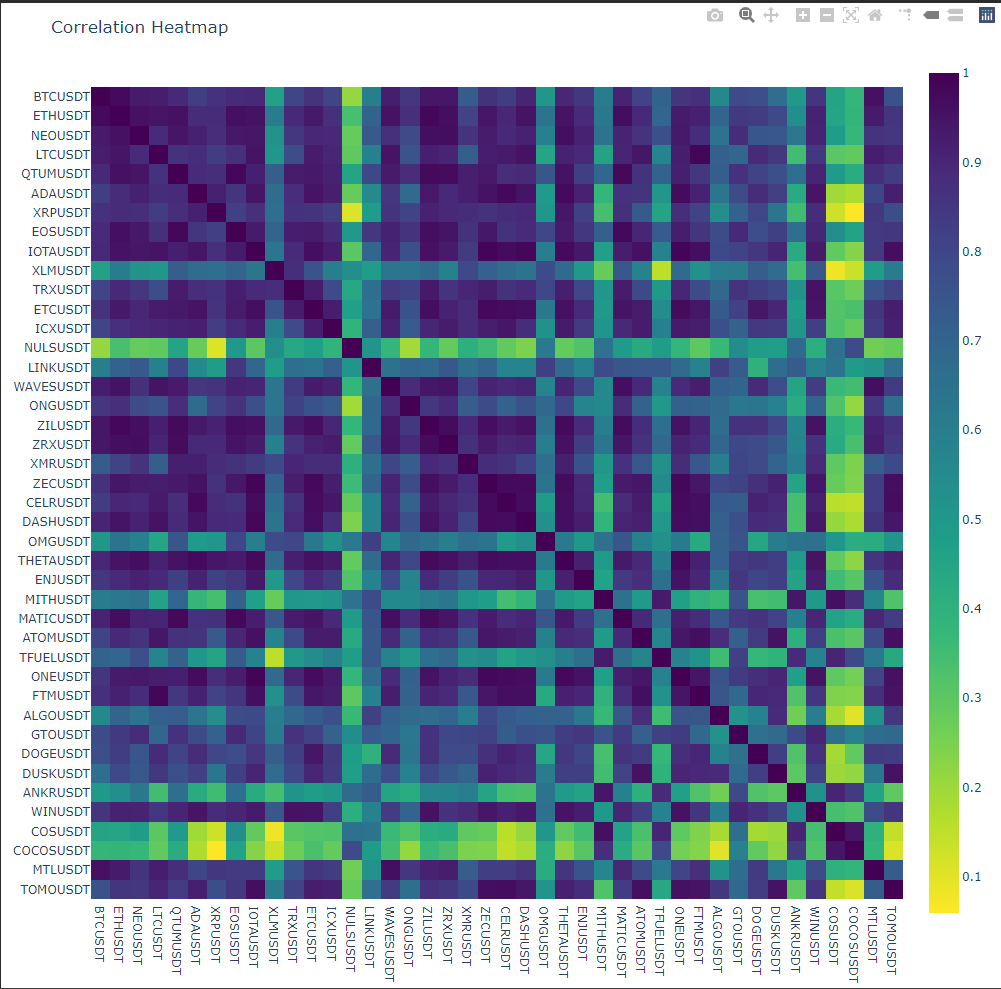

import plotly.express as px

corr = log_df.corr()

fig = px.imshow(corr, color_continuous_scale=px.colors.sequential.Viridis_r)

fig.update_layout(title="Correlation heatmap",

height=1000,

width=1000,

xaxis_nticks=len(corr),

yaxis_nticks=len(corr),

)

fig.show()